Join the Startbutton Community!

Most recent articles

Startbutton vs dLocal: Everything You Need to Know Before Expanding Across Emerging Markets

For any digital business moving into emerging markets, answering the "how" question almost always leads to the same known challenges: do you build your own compliance and payment infrastructure from scratch in every new market, or do you work with a Merchant of Record that already has the legal standing, the local payment rails, and the regulatory relationships in place?

Most founders who have done this before will tell you the answer is the second one. The question then becomes which MoR is suitable for your African expansion, and that's where Startbutton and dLocal enter the conversation.

Both platforms are Merchants of Record; they both serve emerging markets and solve the core problem of cross-border payment complexity. What differentiates them is the different use cases, different organizational sizes, and different geographic priorities they play in. Choosing the wrong one won't just cost you money; it can cost you the market entry window entirely.

This is everything you need to know to make the right call.

First: What a Merchant of Record Actually Does

Let’s be precise about what the MoR model actually changes; contrary to popular opinion, it's not a payment gateway with extra features. The difference is clear.

When you process payments through a standard Payment Service Provider (PSP) like Stripe or Paystack, you remain the legal seller. That means every VAT registration, every tax filing, every chargeback dispute, and every compliance requirement in every single country where your customers live is your responsibility. For a business expanding into five African markets simultaneously, that's a full compliance operation running in parallel to your actual business.

A Merchant of Record steps in as the legal seller on your behalf. It assumes the financial and legal responsibility for every transaction, which includes tax calculation, collection, remittance, fraud liability, chargeback management, and regulatory compliance. You remain the brand the customer interacts with; your checkout still carries your brand identity, but the MoR handles everything that makes the transaction legal, clean, and compliant in all the local jurisdictions you operate in, without having to set up a physical office that needs you to register in all these countries.

PSP | Merchant of Record | |

Legal Seller | Your business | The MoR platform |

Tax Responsibility | You calculate and remit | MoR handles everything |

Local Entity Required | Usually | No |

Fraud and Chargebacks | Your liability | MoR's liability |

Market Entry Time | Months | 24–48 hours |

Setup Cost | $3,000–$10,000+ | Zero upfront fees |

Both Startbutton and dLocal operate as Merchants of Record. Where they differ from each other is in where they operate, how deep their infrastructure goes in specific markets, and which types of businesses they're built to serve.

Startbutton: The Africa-First Compliance Infrastructure

Startbutton was founded in 2023 by Malick Bolakale, formerly of Paystack, and Kelechi Oti, a former Microsoft engineer. That founding team isn't incidental; it's the reason Startbutton's infrastructure reflects how African commerce actually works, not how Western payment systems assume it works.

The platform currently covers 15+ African markets across Anglophone and Francophone Africa, processing over $7 million monthly for more than 200 merchants in sectors ranging from travel and education to gaming and fintech.

The traction-first philosophy

Startbutton's core positioning is what it calls the "traction-first" model: launch in a new market within 24 hours, validate demand, and only commit to locally incorporating once you've hit predefined revenue milestones, typically $10,000 in monthly recurring revenue or a meaningful active user base.

You can also continue transacting with your customers in these countries if the Merchant of Record model is what is most feasible for your team. With Startbutton, customer experience doesn’t become your burden to manage across multiple markets.

Startbutton is deeply customer-centric and takes on the frontline support responsibilities on your behalf—from handling payment-related inquiries, resolving transaction failures, managing refunds and chargebacks, to responding to customer complaints across different regions and currencies.

This means your customers get fast, localized, and compliant support, while your team avoids the operational complexity of building and managing multi-country support systems.

Instead of worrying about fragmented communication, regulatory nuances, or time zone gaps, you can focus on growth, knowing that your customers are being supported seamlessly, and your brand experience remains consistent across every market.

The alternative is expensive and slow. Incorporating a local subsidiary in Nigeria or Kenya costs between $3,000 and $10,000 in legal and administrative fees and takes anywhere from six months to two years. By the time you're operational in the traditional way, your early-mover window has closed. Startbutton lets you generate real revenue and real market data before making that commitment.

Payment rails built for African consumers

This is where Startbutton's founding team background pays its most direct dividend. African commerce doesn't run primarily on international cards; it runs on mobile money, USSD, bank transfers, and domestic card schemes that international processors frequently decline.

Only about 2% of Nigerians own credit cards. Bank transfers account for roughly 22% of transactions. Mobile money platforms like OPay, PalmPay, and Paga represent a growing share. Across Kenya, M-Pesa processed KSh 38.29 trillion in 2025. In Ghana, mobile money interoperability through GhIPSS is the primary retail banking layer for over 26 million active accounts.

Startbutton has direct integrations into all of these: M-Pesa, MTN MoMo, Orange Money, Airtel Money, Verve, Mastercard, Visa, American Express, USSD, and bank transfers across its covered markets. The result is local payment success rates of 80–90%, compared to 25–40% for international card processors attempting to serve the same markets through standard card rails.

Francophone Africa: The strategic expansion

One of Startbutton's most significant moves is its expansion into seven Francophone African countries — Benin, Togo, Mali, Senegal, Guinea Conakry, Burkina Faso, and Cameroon. This region, home to over 300 million people, represents some of the least-penetrated digital commerce markets on the continent.

Critically, Francophone West and Central Africa operate on the CFA Franc, a currency pegged to the Euro and shared across the WAEMU and CEMAC monetary unions. For merchants weary of the currency volatility inherent in the Nigerian Naira or Kenyan Shilling, the CFA zone offers a degree of stability that makes market entry planning significantly more predictable.

African tax compliance as the core product

Startbutton handles Nigeria's SEP rules, where the tax obligation triggers at NGN 25 million in annual digital service revenue from Nigerian users. It automates Kenya's 3% effective SEP tax, calculated by deeming profit at 20% of gross turnover and taxing that at the 30% corporate rate. It manages Ghana's digital monitoring portal requirements and Senegal's zero-threshold VAT registration rule, which requires non-resident digital providers to register from their very first sale.

These aren't edge cases bolted onto a global platform. They're the primary compliance use cases Startbutton was built to solve.

Treasury and settlement

Startbutton allows merchants to collect payments in local currencies — including NGN, KES, GHS, XOF, XAF, UGX, ZMW, and others — and settle in USD, GBP, or stablecoins, such as USDC and USDT, and any preferred local currency, typically within 48 hours. For a business paying cloud infrastructure costs in dollars while earning revenue in Naira, this is a margin protection mechanism, not a convenience feature.

The platform also handles a uniquely African operational reality through its underpayment tolerance feature. Mobile money and bank transfer transactions frequently arrive slightly short of the invoice amount due to network fees or human error. Startbutton allows merchants to configure thresholds that automatically accept and reconcile these payments — eliminating the support tickets and order abandonment that this friction typically creates at scale.

Who Startbutton is built for

Small, mid-market, contract one-time projects, startups, and enterprise-level companies like SaaS and digital product businesses, travel platforms, gaming companies, and fintechs for whom Africa is a primary or significant growth market. Companies that need to move fast, validate demand before committing to local incorporation, Global companies that value their customers and would like to maintain a fast customer relationship that handles issues ranging from fraud, chargebacks, refunds, settlement, and need payment infrastructure that reaches the actual addressable market.

dLocal: The Global Powerhouse

dLocal is a NASDAQ-listed payment infrastructure company operating across 44+ countries across Latin America, Asia, Africa, and the Middle East. Its "One dLocal" philosophy delivers a single direct API, one contract, and one platform to access what it calls the "Global South," and it backs that positioning with institutional scale that few MoR providers can match.

dLocal processes billions in payment volume annually and serves over 600 global merchants, including Shein, Uber, inDrive, and Eneba. Its licensing portfolio covers 30+ jurisdictions, including an FCA license in the UK and MSB registration with FinCEN in the US, the kind of regulatory infrastructure that takes years and significant capital to build.

The dLocal model

dLocal's core value proposition for enterprise merchants is unification. Instead of managing separate payment integrations, compliance frameworks, and settlement structures for Brazil, Nigeria, India, and Indonesia, dLocal consolidates all of that into a single API, a single dashboard, and a single commercial relationship.

That consolidation covers over 900 local payment methods; Pix in Brazil, UPI in India, diverse eWallets across Southeast Asia, mobile money across Africa, and local card rails across Latin America. For a Fortune 500 retailer or a global marketplace that needs genuine multi-regional reach from a single integration, this is genuinely compelling infrastructure.

dLocal for Platforms: Marketplace and gig economy infrastructure

One of dLocal's most differentiated offerings is its specialized solution for complex marketplaces and gig economy platforms. The dLocal for Platforms product enables capabilities that go significantly beyond standard MoR services.

Split payments allow funds to be automatically divided between multiple sellers and the platform in real time. Onboarding automation provides integrated KYC solutions that verify sub-merchants, sellers, and contractors in minutes according to local regulations. Consolidated reporting manages multi-country, multi-currency operations from a single view.

For a ride-hailing company, a freelancer marketplace, or an e-commerce platform where funds need to flow seamlessly between buyers, sellers, logistics partners, and the platform itself — across multiple countries simultaneously, this infrastructure is genuinely purpose-built. It's a level of payment orchestration complexity that most MoR platforms don't attempt.

Enterprise-grade technical infrastructure

dLocal's technical stack is built for high-volume optimization at enterprise scale. Smart Routing directs transactions to the local acquirer with the highest probability of success in real time. Smart Chaining provides fallback routing when primary processors fail. Network Tokenization secures card data for reuse in recurring transactions, reducing fraud exposure and increasing conversion for subscription models.

The platform holds PCI Level 1 status — the highest level of payment card industry compliance — which means enterprise merchants can rely on dLocal's certification rather than building their own, significantly reducing the administrative burden of handling sensitive cardholder data.

dLocal in Africa

dLocal operates in Africa through licensed local entities in key markets. In Nigeria, it operates through Demerge Nigeria Limited, which holds a CBN license as a Payment Solution Service Provider. This institutional standing gives it the legitimacy to handle both B2C and B2B payout flows for large enterprise merchants.

For a company like Shein handling thousands of Nigerian bank transfers and local card transactions as part of a broader global operation, dLocal's standardized interface and enterprise-grade infrastructure is the appropriate tool. It's built for volume, for complexity, and for the kind of institutional accountability that enterprise procurement departments require.

What dLocal costs

dLocal's pricing reflects its enterprise positioning. Card transactions in Nigeria can carry fees of up to 7% for enterprise-tier merchants, with bank transfers at 6%. The dLocal Go product for growing businesses offers more competitive rates at 3.90% for Nigerian cards and bank transfers. Settlement follows a T+1 schedule for enterprise clients, with 3–7 days for Go tier merchants. International wire withdrawals below $20,000 carry a $60 fee.

Who dLocal is built for

Large-scale enterprises and complex marketplaces that need a single infrastructure layer across Latin America, Africa, Asia, and the Middle East simultaneously. Companies with sophisticated marketplace payment needs likee split payments, sub-merchant onboarding, and multi-currency consolidated reporting. Organizations for whom institutional licensing, enterprise SLAs, and a publicly listed counterparty are procurement requirements.

Head-to-Head: The Comparison That Matters

Geographic focus

Startbutton | dLocal | |

Core Focus | Africa (15+ markets) | Global South (44+ countries) |

African Depth | Deep — Anglophone + Francophone | Present — licensed entities in key markets |

LATAM Coverage | Not covered | Primary strength |

Asia Coverage | Not covered | Significant presence |

Francophone Africa | 7 countries and expanding | Limited |

Payment rails

Startbutton | dLocal | |

Mobile Money (Africa) | Native — M-Pesa, MTN, Orange, Airtel, Momo | Supported |

USSD | Supported | Limited |

Local Card Schemes (Verve) | Supported | Supported |

Bank Transfers | All covered markets | Supported |

African Transaction Success Rate | 80–90% | Competitive for enterprise volume |

Compliance and tax

Startbutton | dLocal | |

Nigerian SEP Compliance | Core competency | Handled via local entity |

Kenyan SEP (3% effective rate) | Automated | Managed |

Francophone VAT | CFA zone coverage | Limited |

AML/KYC | African regulatory frameworks | Real-time via international databases |

PCI Level 1 | Yes | Yes |

Licenses and Registrations | African markets | 30+ global jurisdictions |

Pricing

Startbutton | dLocal Enterprise | dLocal Go | |

Card Processing | ~2–3% + $0.50 | 7.00% | 3.90% |

Bank Transfer | ~2–3% + $0.50 | 6.00% | 3.90% |

Mobile Money | ~2–3% + $0.50 | 7.00% | 3.90% |

Settlement Timeline | Within 48 hours | T+1 | 3–7 days |

Withdrawal Fee | Integrated | $60 (under $20,000) | $0 (over $10) |

Setup Cost | Zero | Enterprise contract | Zero |

Stablecoin Settlement | USDC and USDT | Not core offering | |

Setup to First Transaction | As fast as 5 minutes | Structured enterprise onboarding |

The Compliance Reality Neither Platform Can Ignore

Both Startbutton and dLocal exist because the global compliance landscape has fundamentally changed — and the change is accelerating.

Significant Economic Presence rules have decoupled tax liability from physical presence across Nigeria, Kenya, and an increasing number of African markets. A remote SaaS company with meaningful Nigerian revenue now has a Nigerian tax obligation, regardless of where its servers are or whether it has ever registered a local entity. The SEP threshold in Nigeria is NGN 25 million in annual digital service revenue. In Kenya, the obligation begins with the first transaction for non-resident digital providers, at an effective rate of 3% on gross turnover.

Francophone Africa's zero-threshold rule in Senegal is more structured, where non-resident digital providers must register for VAT from their very first sale, with no revenue minimum. If a foreign platform fails to register, the legal obligation to collect and remit VAT shifts to the local payment intermediary. That's the kind of compliance gap that damages infrastructure partnerships and creates retroactive liability simultaneously.

E-invoicing mandates are moving compliance from an annual exercise to a per-transaction requirement. Kenya's eTIMS platform requires real-time invoice submission. Uganda's EFRIS system has expanded across sectors. In these markets, non-compliance doesn't just create a tax problem — it makes your B2B customers unable to claim tax deductions on payments to you, making your product structurally more expensive than compliant local alternatives.

Both Startbutton and dLocal automate these calculations and handle remittance. The difference is depth: Startbutton's compliance engine was built specifically for African regulatory frameworks, while dLocal's compliance infrastructure spans a broader global footprint with correspondingly less market-specific depth in some African jurisdictions.

Industry Use Cases: Which Platform Fits Which Business

SaaS and digital subscriptions

For a SaaS company entering Nigeria, Kenya, or Ghana as its primary growth markets, Startbutton is the natural fit. The traction-first model lets you launch and validate before incorporating. The African tax compliance automation handles SEP and VAT obligations as you scale. And the local payment rail integration ensures you're actually reaching the customers who want to pay you.

For a global SaaS company that already has established operations in Latin America or Asia and wants to add African markets to an existing dLocal integration, the single-platform consolidation argument makes sense at scale.

Travel and hospitality

Startbutton is the trusted MoR for major African travel brands, including Wakanow, specifically because of its ability to handle high-value transfers without the bank red tape that typically delays critical travel-related transactions. For Africa-focused travel platforms, this operational depth matters.

dLocal's installment payment capabilities which make expensive international travel more accessible through monthly payment options are a strong differentiator for global travel brands reaching emerging market consumers across multiple regions simultaneously.

Gaming and digital media

For gaming platforms where speed and micro-transaction reliability are essential, Startbutton's instant payment capabilities and mobile money integration serve the African gaming market effectively. A player topping up their wallet via M-Pesa needs that transaction to clear instantly — friction here is directly correlated with engagement loss.

dLocal's product handles the complexity of distributing payments between developers, publishers, and players across 44+ countries — the right infrastructure for a gaming company with genuinely global distribution needs.

Marketplaces and gig economy platforms

This is where dLocal's advantage is clearest and least contested. The dLocal for Platforms product — with split payments, sub-merchant KYC, and consolidated multi-country reporting — is purpose-built for marketplace complexity. If your business model involves funds flowing between multiple parties across borders, dLocal built specifically for that problem.

The Settlement Question: Protecting Your Margins

Currency volatility isn't an abstract risk in African markets — it's a recurring operational challenge that can quietly erode margins faster than any fee structure.

Startbutton addresses this through USD and stablecoin settlement. Merchants collect in local currencies and receive USD, GBP, USDC, or USDT within 48 hours at the prevailing rate at time of collection. The stablecoin option is particularly relevant as international banks continue de-risking their correspondent relationships with African financial institutions, making traditional SWIFT transfers slower and more expensive. Bypassing the legacy banking system entirely for stablecoin settlement is moving from experimental to practical for high-volume African merchants.

dLocal's Dynamic FX Conversion allows customers to pay in local currency while merchants receive settled funds globally without managing multiple local bank accounts. The T+1 settlement for enterprise clients is strong. The $60 withdrawal fee for transactions below $20,000 is a cost that high-frequency, lower-value payout operations need to factor into their unit economics.

Which Platform Is Right for You?

Choose Startbutton if:

You're a small to mid-market digital business, SaaS company, travel platform, or fintech for whom Africa is a primary or significant growth market. You need to move fast, validate demand before incorporating, and reach the actual addressable market through mobile money, USSD, and local payment rails. You want African tax compliance — Nigerian SEP, Kenyan SEP, Francophone VAT — handled automatically without building a local tax team. And you want USD or stablecoin settlement that protects your margins from local currency volatility, delivered within 48 hours.

Choose dLocal if:

You're a large-scale enterprise or complex marketplace that needs a single infrastructure layer across Latin America, Africa, Asia, and the Middle East simultaneously. You have sophisticated marketplace payment needs — split payments, sub-merchant onboarding, multi-currency consolidated reporting — that require the dLocal for Platforms architecture. Your procurement process requires a publicly listed counterparty, institutional-grade licensing across 30+ jurisdictions, and PCI Level 1 compliance. And Africa is one region within a broader global expansion rather than your primary focus.

Consider both if:

You're a high-growth company with genuine pan-African ambitions and established operations in other emerging market regions. Startbutton handles the African depth. dLocal handles the Latin American and Asian breadth. The two platforms aren't in competition for the same use case — they're complementary infrastructure layers for different geographies.

The Bottom Line

The Merchant of Record model is no longer optional for digital businesses expanding into emerging markets. The compliance landscape has made the DIY alternative — incorporating locally, managing local tax filings, building bilateral payment integrations — genuinely prohibitive for any business that wants to move at the speed the market requires.

The question isn't whether to use an MoR. It's which one was built for your specific expansion?

Startbutton was built for Africa. Its founders came from the heart of African fintech, its payment infrastructure reaches the consumers who actually drive African digital commerce, and its compliance engine was designed for the regulatory frameworks that are catching most foreign businesses off guard. For any company for whom Africa is a serious growth priority, it is the infrastructure layer that makes that priority executable.

dLocal was built for the Global South at an institutional scale. If your expansion spans multiple emerging market regions and your business complexity demands marketplace-grade payment orchestration, it is the most mature unified infrastructure available.

Know your market, know your stage then choose the platform that was built for both.

Read more

Startbutton vs Paddle: Which Merchant of Record Is Right for Your African Expansion?

If you're building a SaaS product or selling digital services and you've started thinking seriously about the Merchant of Record model, you've probably encountered Paddle. It's the established name, well-documented, widely trusted, and genuinely excellent at what it was built to do.

Here's the question that matters for your specific situation: was it built for the market you want to expand to? The merchant of record model promises expansion beyond borders, countries, and markets, but there are also hidden costs to picking the wrong Merchant of record for your business. Poor payment gateways or few payment methods can lead to a high cart abandonment rate for your E-commerce business. Insecure and inflexible payment rails can flag customers as fraudulent, leading to financial losses in global sales, as well as miscalculations in VAT and inadequate AML and KYC processes.

Paddle was designed to solve the global SaaS compliance problem for companies selling into the US, EU, and UK. Startbutton was built specifically to solve the African version of that same problem, a version that is fundamentally different in its infrastructure, its regulatory framework, and the payment methods that actually convert customers. As a 54-country continent, Africa is not a one-size-fits-all kind of market, but rather consists of different countries with different compliance and regulatory requirements, currencies, and policies. Navigating these different environments, if not done properly, can slow down market expansion.

This blog post breaks down both platforms honestly so you can make the right call for where you're expanding.

What is a Merchant of Record, and why does it matter?

Before comparing the two platforms, it's worth being precise about what a Merchant of Record actually does because it's frequently confused with a payment gateway, and the difference is significant.

A Payment Service Provider (PSP), such as Stripe or Paystack, acts as a technical bridge. It moves money from a customer's account to yours efficiently. When you use a PSP, you remain the legal seller. That means you own every VAT filing obligation, every chargeback dispute, every tax registration requirement in every country where your customers live. For a company expanding across multiple markets simultaneously, that's a full-time compliance operation that has nothing to do with building a product.

A Merchant of Record steps in as the legal seller on your behalf. It assumes responsibility for tax calculation, collection, and remittance; fraud liability and chargeback management; and regulatory compliance across every market it covers. You remain the brand the customer interacts with. The MoR handles everything that happens around the transaction to keep it legal, clean, and compliant.

PSP | Merchant of Record | |

Legal Seller | Your business | The MoR platform |

Tax Responsibility | You calculate and remit | MoR handles everything |

Fraud and Chargebacks | Your liability | MoR's liability |

Local Entity Required | Usually | No |

Setup Time | Weeks to months | Hours to days |

Both Paddle and Startbutton operate as Merchants of Record. The difference is in where they operate and how they've built their infrastructure to serve their target markets.

Paddle: The Global SaaS Standard

Paddle has been building its MoR infrastructure for over a decade and processes approximately $6 billion in Total Payment Volume annually. Its value proposition is to remove the operational friction of global SaaS compliance, allowing founders to focus on product development and customer acquisition.

What Paddle does well

Paddle's tax engine covers over 200 countries and handles the full compliance lifecycle, including automatic rate calculation based on customer location, registration in more than 100 jurisdictions, periodic filing, and remittance. For a SaaS company selling to customers in the US, EU, and UK, this is genuinely comprehensive coverage.

Its acquisition of ProfitWell integrated a significant data layer into the platform, real-time MRR tracking, churn analysis, cohort analytics, and LTV calculations, all included as a free service. The Retain product adds automated dunning and churn intervention using machine learning, with reported recovery rates of up to 30% of failed payments. For a subscription business where retention is the primary revenue lever, this is a meaningful differentiator.

Pricing is straightforward: 5% + 50¢ per transaction. When you factor in what a DIY stack costs, tax software, currency conversion, churn recovery tools, Paddle's all-in fee often comes out cheaper in effective rate terms.

Where Paddle falls short for African markets

Paddle was not built for Africa, and its infrastructure reflects that honestly.

Payment method coverage is primarily card-based, including Visa, Mastercard, and a selection of local card methods for Western markets. Mobile money, which is the primary payment method for the majority of consumers across Nigeria, Kenya, Ghana, and beyond, is not a core part of Paddle's infrastructure. M-Pesa, MTN MoMo, Verve, and Orange Money are not natively supported.

This is not a minor gap that shouldn’t be ignored. International card processors attempting to serve African markets typically see transaction success rates of 25–40% due to fraud detection filters that don't account for local spending patterns. For a business whose African customers primarily transact via mobile money, Paddle's infrastructure creates a ceiling on conversion that no amount of checkout optimization will overcome.

On the tax side, Paddle's expertise is built around OECD frameworks, US sales tax, EU VAT, and post-Wayfair economic nexus thresholds. Africa's specific compliance mechanisms, Nigeria's Significant Economic Presence rules, Kenya's 3% SEP tax on digital services, Ghana's digital monitoring framework, Senegal's zero-threshold VAT registration requirement — are not what Paddle's engine was designed to navigate.

Startbutton: built for the African Infrastructure reality.

Startbutton was founded in 2023 specifically to dismantle the cross-border barriers that prevent digital businesses from scaling across African markets. It currently covers 15+ African markets, including Nigeria, Kenya, Ghana, Rwanda, South Africa, Zambia, and seven Francophone countries, and processes over $7 million in monthly transactions for more than 200 merchants.

What Startbutton does well

Payment rails that actually work in Africa. Startbutton has direct integrations into the local payment infrastructure that powers African commerce — M-Pesa, MTN MoMo, Orange Money, Verve, USSD, and bank transfers across its covered markets. This isn't a card overlay with mobile money bolted on. Its infrastructure was built from the ground up for how African consumers actually pay. The result is local payment success rates of 85–90%, compared to 25–40% for international card processors attempting to serve the same markets.

African tax compliance as a core competency: Startbutton handles the specific compliance mechanisms that define digital taxation across Africa — Nigeria's NGN 25 million SEP threshold, Kenya's 3% effective SEP tax rate on gross digital service turnover, Ghana's digital monitoring portal requirements, and the zero-threshold VAT registration rules in Francophone markets like Senegal. These aren't edge cases in Startbutton's compliance engine. They're the primary use case it was designed to serve.

Treasury and FX management: Currency volatility is one of the most persistent operational challenges for businesses earning in African local currencies. Startbutton's settlement infrastructure allows businesses to collect in NGN, GHS, KES, or any other local currency and settle in USD or GBP, typically within 48 hours. For a business paying cloud infrastructure costs in dollars while earning revenue in Naira, this is not a convenience feature. It's a margin protection mechanism.

Speed to market: A traditional market entry into Nigeria or Kenya — local incorporation, bank account setup, tax registration, payment integrations — takes between six months and two years and costs $3,000–$10,000 in legal and administrative fees before you've served a single customer. Startbutton compresses this entire process into 24–48 hours through a single API integration, while also providing localized customer support for African time zones, along with chargeback and fraud management.

Built for African market realities: Startbutton’s product is built with the operational nuances of African markets in mind, where mobile money transactions often arrive slightly below the intended amount due to network fees or human error. A payment of NGN 99,950 instead of NGN 100,000 may seem minor, but at scale, it creates significant reconciliation challenges.

To solve this, Startbutton’s underpayment feature allows merchants to set tolerance thresholds that automatically accept and reconcile these transactions, reducing support overhead and preventing unnecessary order abandonment.

Where Startbutton's focus differs from Paddle

Startbutton's strength is geographic and infrastructure depth, not the breadth of subscription analytics tools. If your primary need is sophisticated dunning software, MRR cohort analysis, or churn prediction ML models, that's Paddle's territory. Startbutton is built for the merchant who needs reliable payment collection, tax compliance, local currency conversions, and USD settlement across African markets, not only for the SaaS CFO optimizing subscription revenue metrics for a Western customer base, but also for the Fintech, Edutech, Gaming, E-commerce, Digital Products, HRaaS, Travel, Remittance, Forex, and Payment operators

Head-to-head: The Key comparison points

Geographic coverage

Paddle | Startbutton | |

Core Markets | US, EU, UK, APAC | 15+ African markets |

African Coverage | Limited | Nigeria, Kenya, Ghana, Rwanda, South Africa, Zambia + Francophone |

Market Entry Time Business type | Days (for supported markets) SaaS | 24–48 hours, depending on how complete your Business documents are Fintech, Edutech, Gaming, E-commerce, Digital Products, HRaaS, Travel, Remittance, Forex, Financial services. |

Payment methods

Paddle | Startbutton | |

Cards | Visa, Mastercard, local EU/US methods | Cards supported |

Mobile Money | Not supported | M-Pesa, MTN MoMo, Orange Money, Airtel |

USSD | Not supported | Supported |

Bank Transfers | Limited | Supported across all markets |

Transaction Success Rate (Africa) Payout speed & reliability | 25–40% | 80–90% |

Tax and compliance

Paddle | Startbutton | |

Tax Expertise | OECD, US, EU VAT | African DST, SEP, regional VAT |

Nigeria SEP Compliance | Not specialized | Core competency |

Kenya SEP (3% effective rate) | Not specialized | Automated calculation and remittance |

Francophone VAT | Not specialized | CFA Franc zone coverage |

AML/KYC | Standard | Built for African regulatory frameworks |

Settlement and treasury

Paddle | Startbutton | |

Settlement Frequency | Monthly | Real-time or batch (within 48 hours) |

Settlement Currency | USD, EUR, GBP | USD, GBP, or local currencies like GHS, NGN, KES, XOF, XAF, UGX, etc |

FX Management | Standard global rates | Real-time FX via API at time of collection |

Local Currency Trapping | Not applicable | Solved via treasury infrastructure |

Pricing

Paddle | Startbutton | |

Fee Structure | 5% + 50¢ per transaction | Depends on the country, (~2–4%) |

Setup Cost | Zero upfront | Zero upfront |

Hidden Add-ons | Minimal | Minimal |

The Tax Compliance detail that catches most founders off guard

Africa's digital tax landscape has changed faster than most expansion playbooks account for. Two specific mechanisms are worth understanding in detail before you launch.

Nigeria's Significant Economic Presence (SEP) rule creates a tax obligation for non-resident digital businesses once they cross NGN 25 million in annual revenue from Nigerian users. This means your Nigerian traction, the thing you've been working to build, is what triggers the compliance requirement. The obligation doesn't wait for you to open a local office.

Kenya's SEP tax is calculated by deeming profit at 20% of gross turnover and taxing that deemed profit at Kenya's 30% corporate rate, producing an effective tax rate of 3% on gross digital service revenue. With no threshold for non-resident providers, the obligation begins when your first Kenyan customer pays you.

Ghana's VAT regime doesn't have a single clean trigger like Nigeria's NGN 25 million threshold, but it has layers. The standard VAT rate sits at 15%, but once you add the NHIL and GETFund levies on top, the effective rate a foreign digital business is working with is closer to 20%. Non-resident digital service providers must register with the Ghana Revenue Authority once they cross the GHS 750,000 annual revenue threshold. Cross it, and registration isn't optional.

What makes Ghana's approach distinct is that the GRA is actively deploying digital monitoring infrastructure specifically designed to track cross-border digital transactions, meaning the question isn't whether they'll eventually see your Ghanaian revenue, but whether your compliance infrastructure will be ready when they do.

South Africa runs one of the most precisely enforced digital tax authorities on the continent. The rule is simple: once a foreign electronic service provider crosses R1 million in annual revenue from South African customers, VAT registration with SARS is compulsory. No grace period, no discretion.

The VAT rate is 15%, scheduled to move to 15.5% in 2025 and 16% in 2026, and SARS enforces it with a level of administrative sophistication that more closely resembles a European tax authority than what most founders expect from an African market. South Africa has also passed the Global Minimum Tax Act, implementing the OECD Pillar Two framework and setting a 15% effective tax floor for large multinationals. If your offshore holding structure was designed to minimize South African tax exposure, that architecture deserves a fresh look.

Senegal's DGID runs the sharpest compliance edge in Francophone Africa, and the one that catches the most foreign founders off guard. There is no revenue threshold. Non-resident digital providers must register for VAT from their very first sale into the Senegalese market. Not after $10,000 in revenue. Not after 1,000 users. Transaction one.

The VAT rate is 18%, and the enforcement mechanism makes non-compliance particularly costly to sidestep. Under Article 355 bis of Senegal's tax code, if a foreign platform fails to register, the obligation to collect and remit VAT shifts directly to the local payment intermediary — meaning your payment gateway becomes liable for the tax you didn't collect. That's the kind of compliance gap that damages infrastructure partnerships fast.

Côte d'Ivoire implemented mandatory e-invoicing for all B2B and B2C transactions via its FNE platform as of September 2025. For any foreign digital business with Ivorian customers, that mandate applies regardless of where your entity is registered. The 2026 budget goes further, proposing a 30% SEP tax on digital business profits, capped at 10% of revenue generated from Ivorian consumers. That cap is the detail worth paying attention to: it limits your maximum exposure, but it also means the obligation is calculated on gross revenue, not net profit.

Startbutton automates both calculations and handles remittance to the relevant authorities. For a lean team trying to build in multiple markets simultaneously, automation isn't a nice-to-have. It's what keeps a compliance oversight from becoming a fundraising complication.

Who should use Paddle?

Paddle is the right choice if your primary customers are in the US, EU, or UK; your product is a SaaS or digital subscription; your customers pay primarily by card; and you want subscription analytics, churn management, and dunning automation integrated directly into your billing infrastructure.

It is not the right choice if your African customers are a meaningful part of your revenue or growth strategy, or if mobile money is a primary payment method for the users you're trying to serve.

Who should use Startbutton?

Startbutton is the right choice if you're expanding into African markets and need payment infrastructure that actually reaches your addressable market; if mobile money, USSD, or local bank transfers are how your target customers transact; if you need automated compliance for African-specific tax regimes like SEP and DST; or if currency volatility and FX settlement are operational concerns for your business.

It is not a replacement for Paddle's subscription analytics suite or its depth of coverage in Western markets.

Do you have to choose?

For companies with genuine pan-African and global ambitions, the answer may simply be both. Paddle handles the established Western markets where card-based checkout is standard, and Startbutton handles the African markets where the infrastructure reality is fundamentally different.

The MoR model's core value is that it handles the compliance layer so you can focus on growth. Using the right MoR for each geography isn't operational complexity — it's operational clarity. You're not building a custom compliance stack for 20 different markets. You're using two specialized platforms, each excellent at what it was built for, to cover the markets that matter to your business.

The Bottom Line

Paddle is a mature, well-built platform for global SaaS companies with a primary focus on Western markets. If that's your situation, it's hard to argue against it.

But if Africa is where your next chapter of growth is happening or where it should be, you need infrastructure that was built for the continent's actual payment landscape, not adapted from a Western model that doesn't translate to real-time growth and revenue.

Startbutton exists specifically for that problem, and for any business serious about pan-African expansion, it's the infrastructure layer that makes the ambition executable.

Read more

How to Refund a transaction on the Startbutton dashboard

Refunds are part of scaling. Customers change their minds, duplicate payments happen, and sometimes you need to correct an under/overpayment.

Startbutton makes this easy by letting you initiate full or partial refunds for collections done via Virtual Accounts (VA), Card, and Mobile Money (MoMo) right from your dashboard or via API.

This guide shows you where to find the transaction, how to initiate the refund, and what the confirmation looks like afterward.

To issue a refund smoothly, confirm these first:

You’re in the correct currency/account on your merchant dashboard (refunds are initiated from the account where the collection was made).

Your available balance is sufficient to cover the refund amount (for the amount you’re trying to refund).

You know whether you’re doing a full refund or a partial refund.

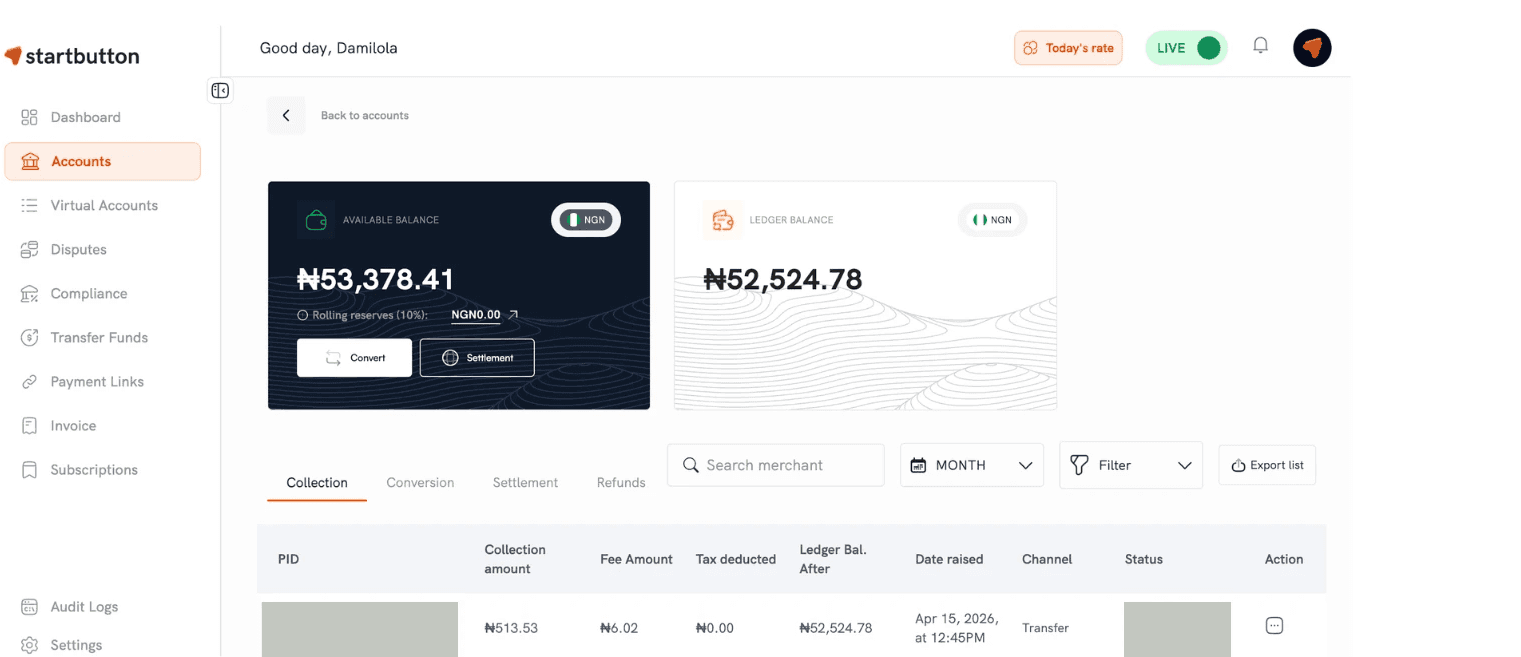

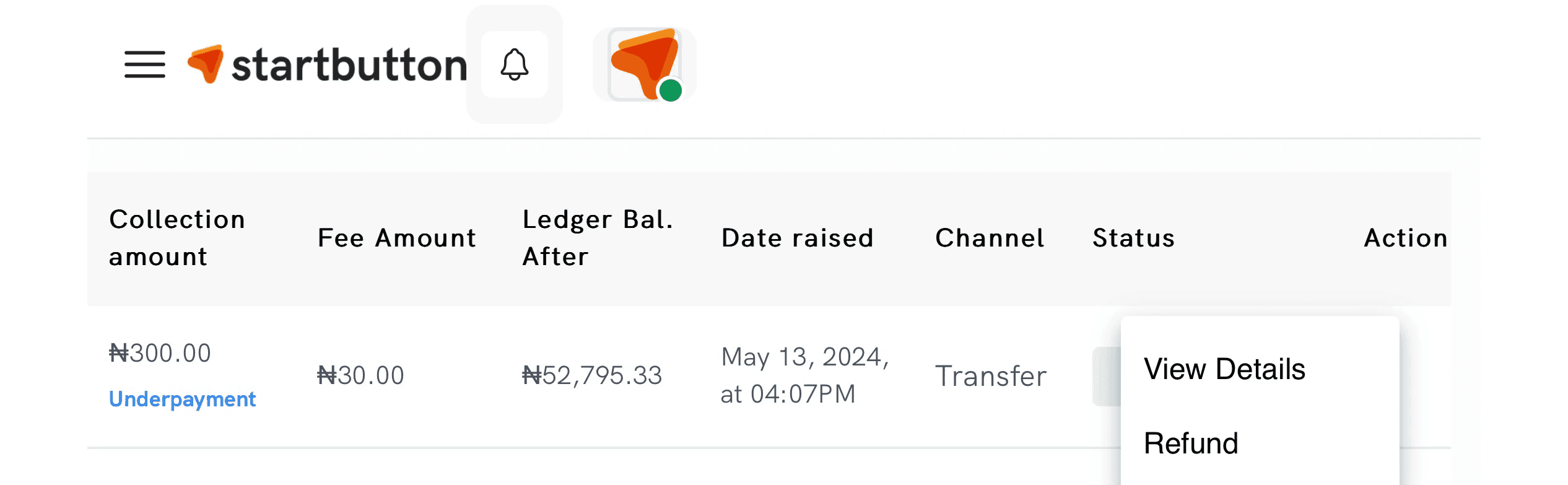

Step 1: Find the transaction you want to refund

Option A: Find it from your Transactions table

Log in to your Startbutton Dashboard.

Select the currency/account the payment was received in.

Go to Transactions.

Search or filter until you find the transaction you're looking for.

Option B: Use the transaction details view to confirm you’ve got the right one

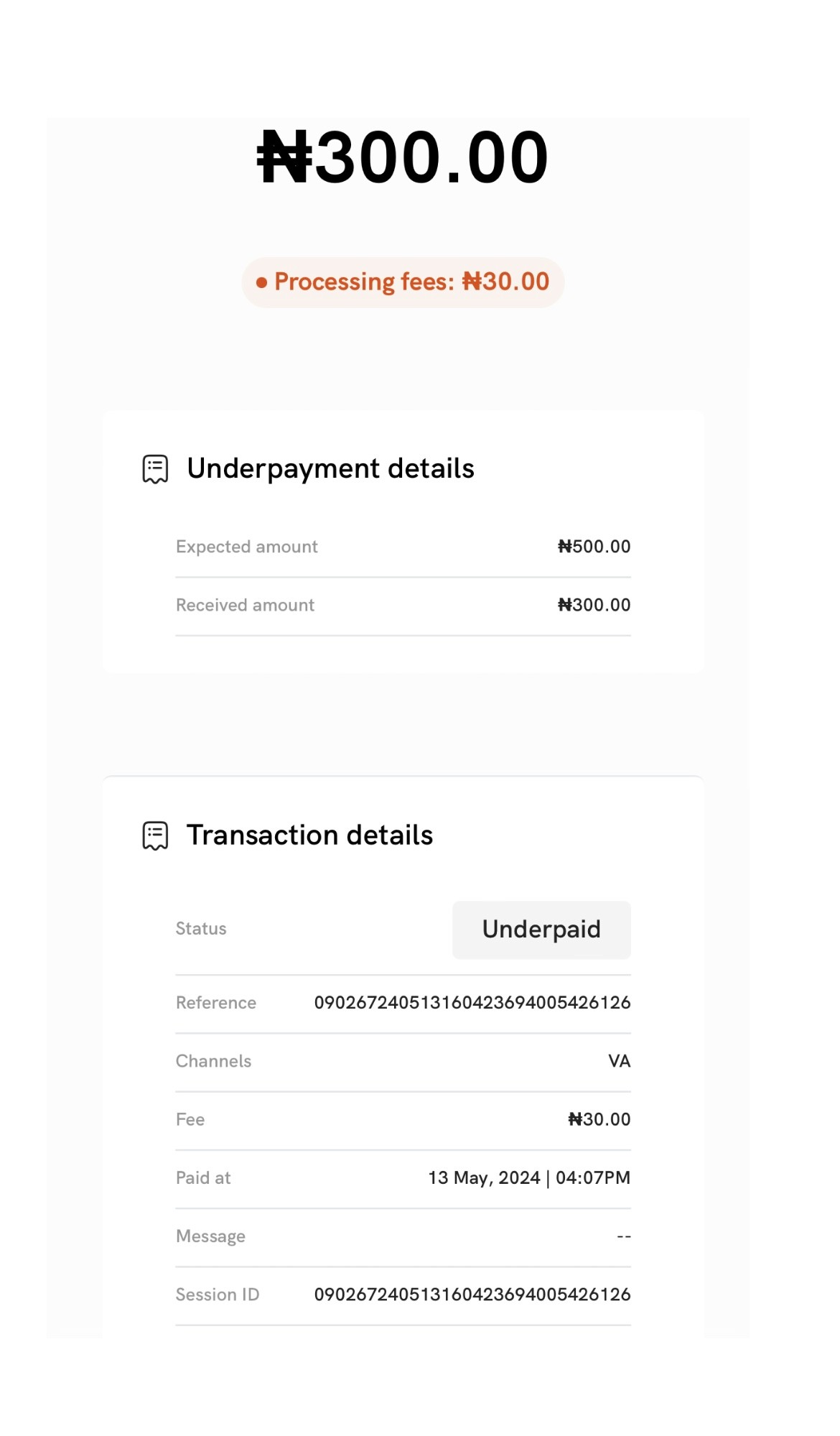

Open the transaction and use View detail to confirm the amount collected, payment channel (VA/Card/ MoMo), and the reference number that helps you reconcile

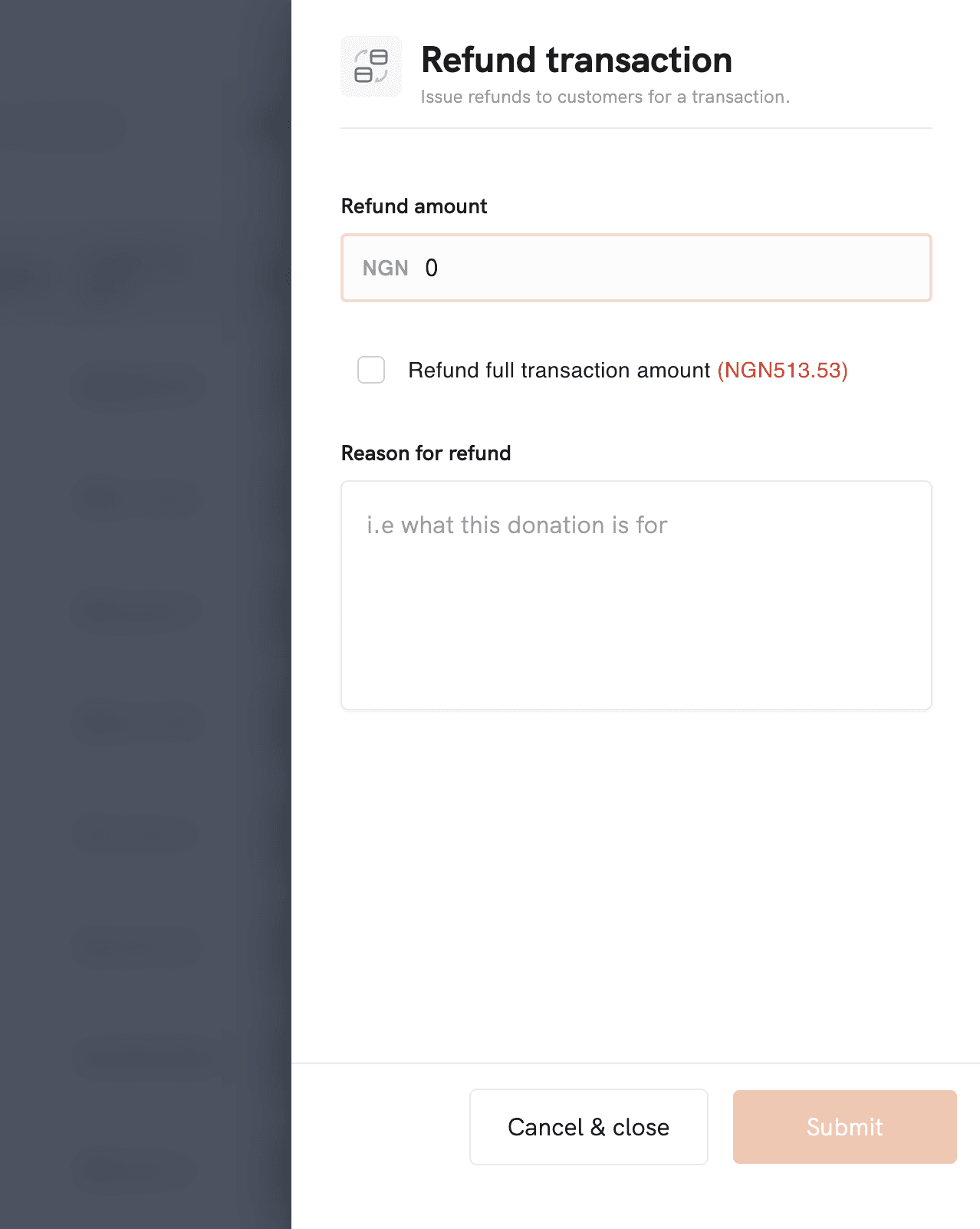

Step 2: Initiate a refund (Dashboard)

Refunds can be initiated from your dashboard in a few clicks:

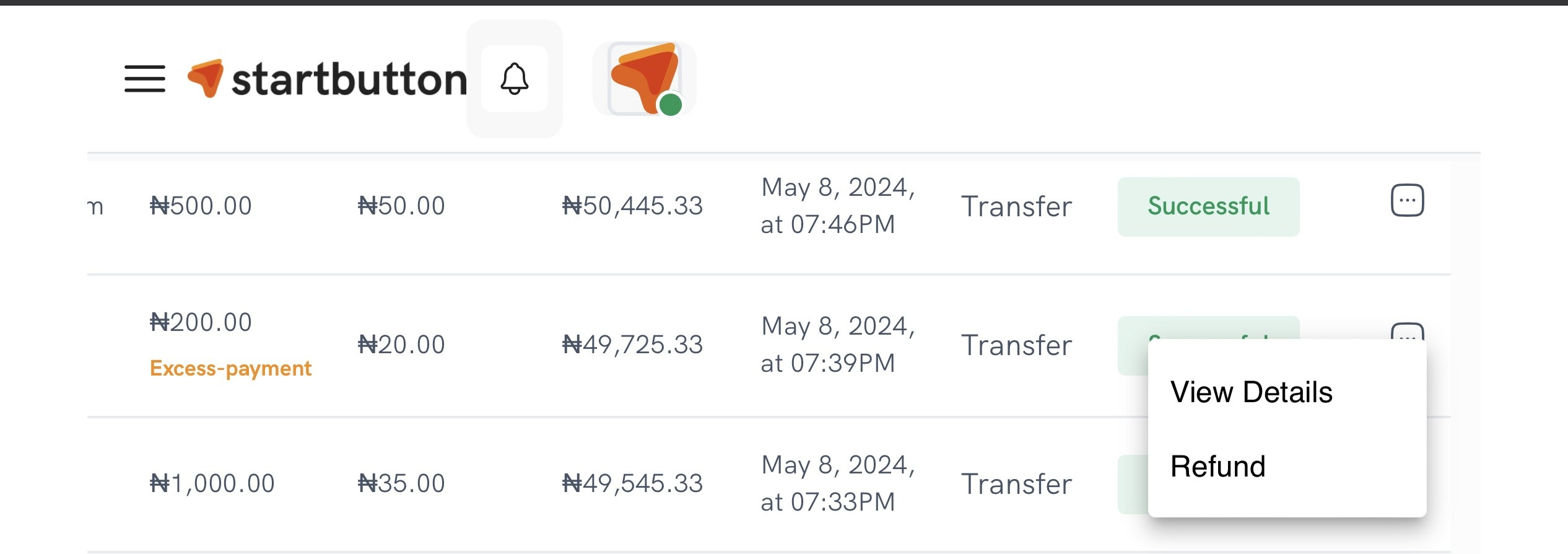

In your Transactions table, locate the transaction.

Click the Action (… ) button.

Select Refund.

In the refund dialog:

Enter the amount (full or partial)

Add a reason

Click Submit to initiate the refund.

You can’t enter an amount higher than the original transaction amount.

Refunds can be partial or full.

Step 3: What confirmations look like (after you submit)

Once a refund is initiated, Startbutton gives you two main forms of confirmation:

1) Email confirmation

When a refund is processed, you receive an email indicating whether the refund was successful or failed.

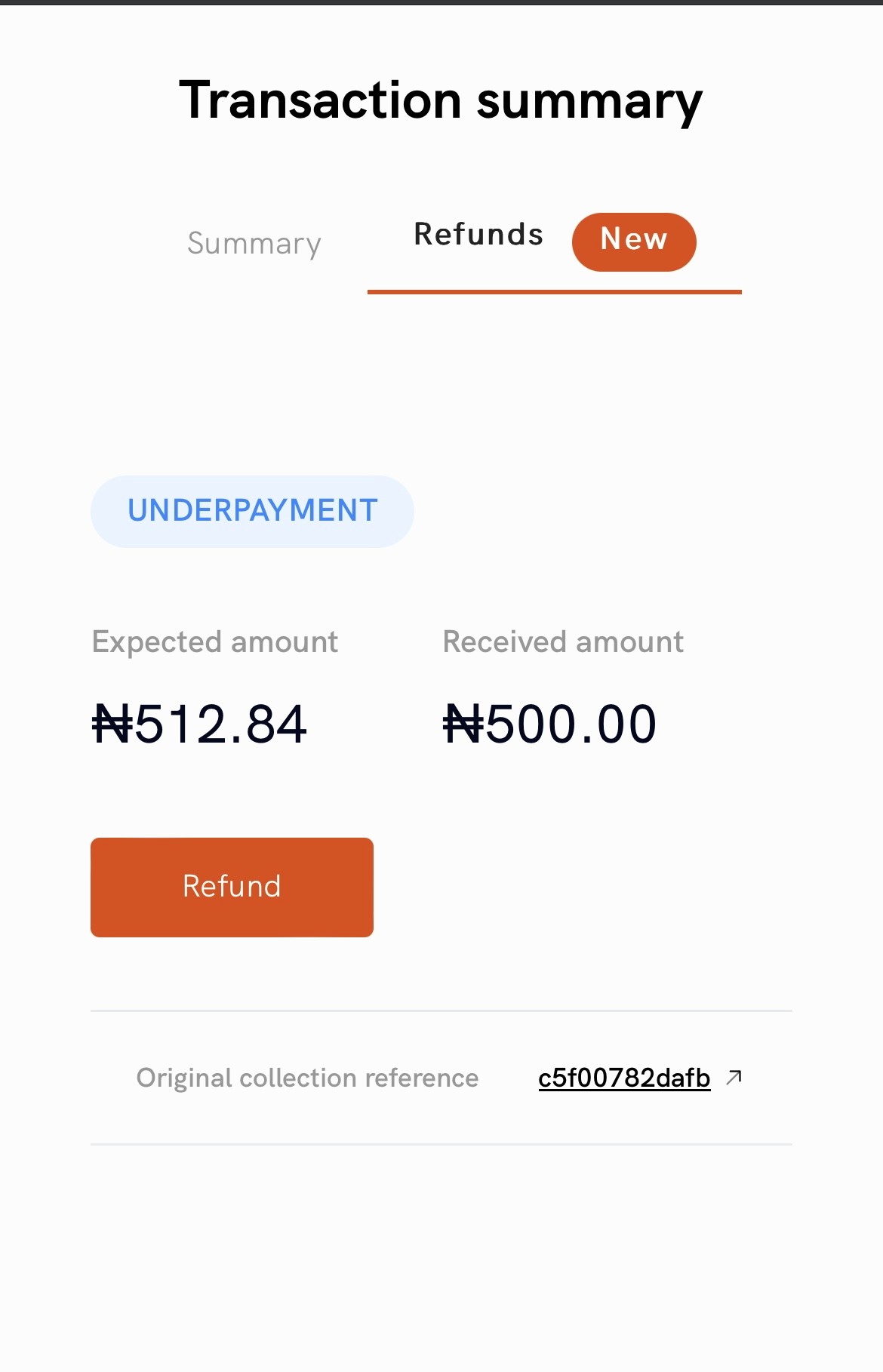

2) Refunds tab + receipt view

To track refunds on your dashboard:

Navigate to the account/currency where you initiated the refund.

Open the Refunds tab.

In the Refunds table, you’ll see fields such as:

Refund reference

Collection reference

Collection amount

Refunded amount

Date

Origin (Dashboard)

Status (success / failed / pending)

To see the full confirmation details, click View receipt to view:

the original transaction details

the refund transaction details + status

From a workflow standpoint, the refund experience is the same:

The key difference is simply the payment channel the original collection used (VA, Card, or MoMo). The dashboard flow stays consistent.

Common scenarios (and how to handle them)

Scenario 1: Customer requests a full refund

Refund the full amount.

Track status in the Refunds tab.

Scenario 2: Customer needs a partial refund

Example: customer paid 50,000, but you need to return 10,000.

Initiate a refund for 10,000.

Your Refunds table will show the refunded amount and status.

Scenario 3: Underpayment/overpayment cleanup

If a transaction is tagged as an underpayment or excess payment, you can still refund it as part of correcting the discrepancy.

API option (for teams that want to automate refunds)

Refunds can also be initiated via API.

At a high level:

You provide the original transaction reference (to identify what’s being refunded).

You provide the amount (full or partial).

You can query refund status with the Refund TSQ endpoint.

FAQs

Can I refund partially?

Yes. Refunds can be partially or fully initiated.

Where do I see the refund status?

On the dashboard, go to the Refunds tab for the relevant currency/account. You’ll see statuses like success/ failed/pending, and you can open the receipt for details.

Will I get notified after I initiate a refund?

Yes. You’ll receive an email telling you if the refund was successful or failed.

Can I refund an underpayment or excess payment?

Yes, refunds also work for transactions tagged as underpayment or excess payment.

Read more

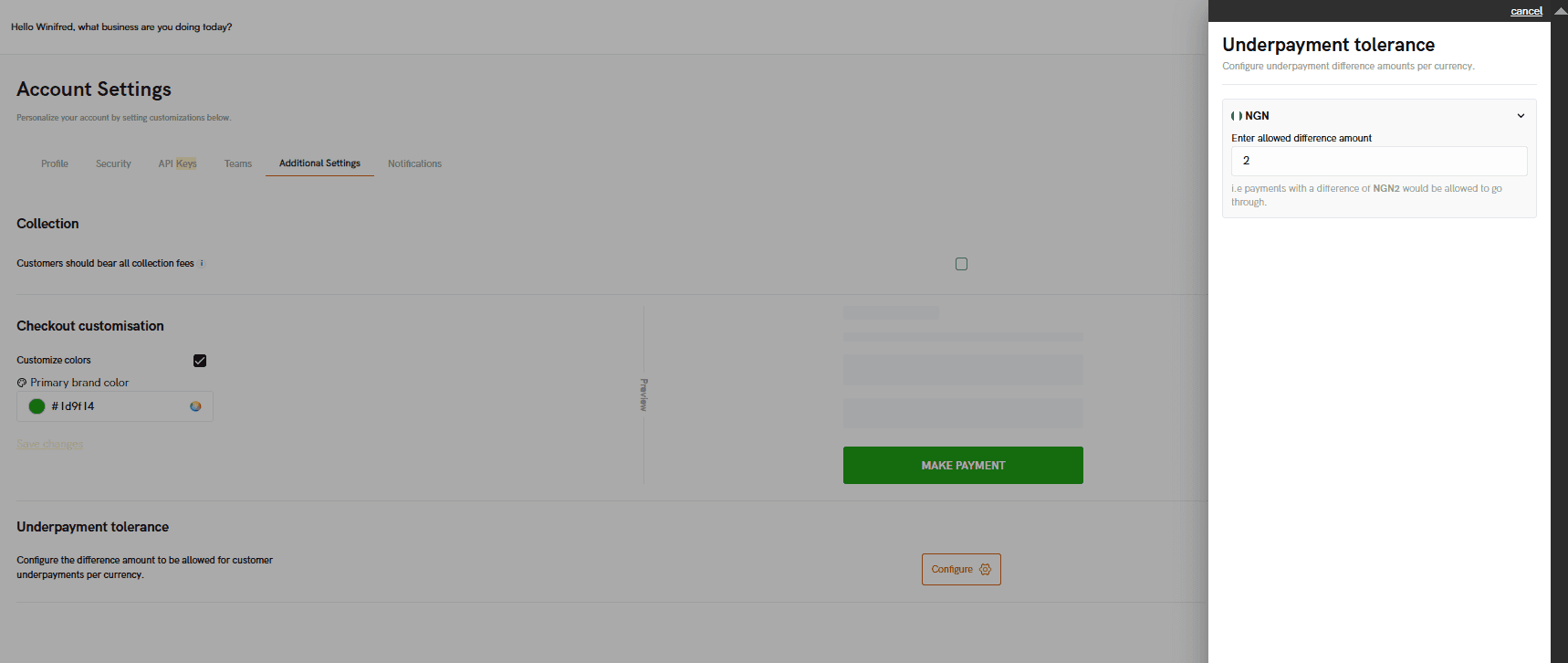

How to use the Underpayment Tolerance feature

Underpayments happen when customers pay less than the expected amount, most commonly when paying via bank transfer and typing an amount manually. If you process a lot of transfers, small amount shortages like ₦50, ₦200, or ₦1,000 can quickly turn into hours of manual follow-ups and reconciliation.

Underpayment Tolerance feature helps you decide what’s acceptable versus what should be rejected automatically.

What is Underpayment Tolerance?

Underpayment Tolerance is a merchant-controlled setting that defines the maximum underpayment difference you’re willing to accept (a flat amount) per currency.

Once it’s set:

Payments that are underpaid by more than your tolerance are automatically rejected (bounced/reversed).

Payments that are underpaid by less than or equal to your tolerance are accepted and tagged as underpaid for easier reconciliation.

You can configure it directly from your Startbutton Merchant Dashboard:

Log in to your Startbutton Dashboard

Go to Settings

Click on "Additional settings" on the top bar to "configure" the Underpayment Tolerance section

Set a flat threshold amount per currency

Click on Save

How it works with practical examples

Example 1: Small underpayment

A customer is meant to pay ₦100,000 but sends ₦99,950.

If your operations can’t tolerate discrepancies, request a top-up or refund, and request a new payment.

If you’ve set a tolerance and the shortage is within your acceptable range, accept and reconcile with your team.

Example 2: Large underpayment

A customer is meant to pay ₦100,000 but sends ₦60,000.

Most businesses do not fulfill.

Either request a new payment for the full amount (then refund the ₦60,000) or follow your support workflow.

Example 3: Overpayment

A customer is meant to pay ₦100,000 but sends ₦120,000.

Confirm the overpayment tag/excess amount.

Refund the extra ₦20,000 (or refund the full amount and request a clean re-payment for strict workflows).

How Underpayment tolerance affects reconciliation

Underpayment Tolerance improves reconciliation in two ways:

1) It reduces “clutter” in your transaction list: Instead of accepting every small underpayment and forcing your team to review and decide what to do, transactions that fall outside your tolerance are blocked automatically.

2) It makes the remaining underpayments intentional and easier to track: For underpayments you accept (within tolerance), tagging makes it easier to:

identify discrepancies quickly

match them to the expected/initiated transaction

decide the next step (top-up request, partial fulfillment, or refund)

What to do when a customer underpays

Step 1: Check the transaction tag and details

Confirm the expected amount, the received amount, the shortage, and whether it was accepted (within tolerance) or rejected (above tolerance)

Step 2: Choose your business outcome. Common merchant policies ranges from

Request a top-up for the outstanding difference

Provide value partially (only if your business supports partial delivery)

Refund the received amount and ask the customer to retry with the correct amount

Step 3: Use transaction details to trace the original context

When a payment is tagged as underpaid, you can use the transaction details view to retrieve the “original” transaction context (like the expected reference/order context), which helps your Ops/Support team communicate clearly with the customer.

Step 4: Initiate a refund if needed

Refunds can be initiated via:

The Merchant Dashboard

The Refunds API

(You can refund the full amount, or set an amount for partial refunds depending on your workflow.)

Recommended setup guidelines (how to choose a threshold)

Your best threshold depends on what underpayments look like in your business. A practical way to decide:

If your typical order value is low and margins are tight, use a strict tolerance (small number).

If your typical order values are high and customers occasionally miss small amounts, use a slightly higher tolerance, but keep it low enough to avoid abuse.

Also consider:

How much time does your support team spend resolving underpayments?

Do you support partial value delivery?

Whether fees/charges commonly cause small “mistyped amount” discrepancies

FAQs

1) Do I still need to contact Startbutton support to set this up?

No, you can set, view, and update Underpayment Tolerance directly from your dashboard settings.

2) Is the tolerance the same for every currency?

No. You can set a different value per currency (depending on what’s available for your account/currencies).

3) What happens when a customer underpays above my tolerance?

The payment is rejected (bounced/reversed). You don’t receive the funds.

4) What happens when a customer underpays within my tolerance?

The payment can be accepted and tagged as underpaid, so you can reconcile and decide next steps

5) Can I set the tolerance to Zero?

Yes. Setting it to 0 means you’ll accept all underpayments (i.e., no automatic rejection based on tolerance).

6) Does this apply to all payment methods?

Underpayment Tolerance is most relevant for bank transfers, where customers manually enter an amount, and discrepancies are common.

Read more

How to handle Under & Over Payments transactions

Payment discrepancies happen, and they’re more common than you think. A customer may send less than the amount you requested, or send more than expected. Either way, you’re left with questions like, Is the order fully paid for? Should you give value since the amount received is less than the intended cost of the service or product? How do you reconcile it quickly? What do you refund (and how)?

This guide breaks down what underpayments and overpayments are on the Startbutton dashboard, what happens when they occur, and the practical steps to resolve them without slowing down your business.

What counts as an underpayment vs. an overpayment?

When a customer pays via bank transfer, Startbutton compares the expected/initiated amount (what the customer was meant to pay) to the received amount (what actually hit the account)

If the received amount does not match the expected amount, Startbutton categorizes the payment:

Underpayment: the received amount is below the expected amount.

Overpayment (excess payment): the received amount is above the expected amount.

How to handle an underpayment

Step 1: Confirm the discrepancy, check the transaction details, and compare the initiated amount, the received amount, and the difference.

Step 2: Decide the business outcome. Most businesses use one of these policies:

Strict policy: do not provide value until the full amount is received.

Grace policy: Provide value if the shortage is small and within an acceptable tolerance.

Refund policy: refund the payment if it can’t be completed or will cause operational issues.

Step 3: Click on "Dashboard" or "Account" in the left menu corner to locate the underpaid transaction currency.

Step 4: Use “View details” to find the original reference. For underpaid transactions, you can locate the original transaction reference/order number from the transaction details.

Step 5: Click the […] action menu beside the transaction status row, Open the transaction by clicking on "View details" to confirm the reference number

Step 6: Go back to Click on "Refunds" to initiate the refund process, you can initiate a refund from:

Dashboard (manual)

API (programmatic)

If you specify an amount, you can do a partial refund; if you leave the amount blank (API), Startbutton refunds the full amount.

How to handle an overpayment

Step 1: Confirm if it’s truly an overpayment

Overpayments are often caused by customers typing the wrong amount, duplicated transfers, or misunderstanding the fee breakdown

Step 2: decide what you want to do with the excess

Refund the excess (most common)

Keep as wallet credit (if your business supports it and has consent)

Refund the full amount and request a clean re-payment (for high-risk cases)

Step 3: Use “View detail” to retrieve the original reference number

Step 4: Initiate the refund. Refunds can be initiated via:

dashboard action button (Refund)

API refund endpoint

When initiating a refund from the dashboard, you’ll typically:

Select the transaction

choose Refund

Enter the refund amount (full or partial)

Enter a reason

submit

The Transaction receipt looks like the image below

Note: You can’t refund more than the transaction amount, and you’ll be able to track refunds from the Refunds tab for the currency/account used

If your business frequently receives “random small differences” (e.g., ₦50 shortfalls), you can reduce noise by using Underpayment Tolerance.

Why this matters (and what it can break)

Under & over payments can create real operational friction. During reconciliation days, your finance team is delayed by spending valuable time matching bank transfers to orders, customers insist they’ve paid even when the amount is clearly off, and your dashboards and accounting exports become harder to trust due to inaccurate reporting of transactions and services provided.

The goal is simple: detect the discrepancy early, keep your records clean, and resolve the difference quickly. When an underpayment or overpayment occurs, Startbutton helps by doing three things:

Tags the payment so it’s easy to spot during reconciliation.

Keeps the transaction traceable by making it possible to find the “original” transaction reference/order context.

Enable refunds so you can return funds (either the full amount or part of it), depending on your resolution path.

Frequently asked questions

1) Can I refund an underpayment or excess payment?

Yes. Refunds can be initiated for transactions tagged as underpayment or excess payment.

2) Can I refund partially?

Yes. You can specify a refund amount (dashboard), and via API, you can optionally set the refund amount; leaving it blank triggers a full refund.

3) Do I get notified when discrepancies happen?

Discrepancies can be tagged, and you can receive webhook notifications (depending on your integration and event configuration).

4) Does this apply to every payment method?

The core under/over payment flow is designed for bank transfer transactions where customers manually input the amount.

Read more

The different ways to expand your digital company

Every founder hits the same moment eventually. The home of the business residence market is working; revenue is growing. The product has clearly earned real trust. Then, someone, an investor, a board member, or an employee, or maybe just the data, starts asking the obvious question: what's next?

International expansion is the most common answer, but "expand internationally" is not a strategy. The strategy is everything that comes after: the how, the where, the when, and the infrastructure that determines whether crossing a new border accelerates your business or quietly drains it.

Here are the different ways to expand a digital company, and the right model that makes each of them actually work effectively as they should.

1. Direct market entry with a local entity

The most traditional path is to incorporate a subsidiary of your company in the targeted market, hire locally, open bank accounts, register for taxes, and build your presence from the ground up as a legal entity in that country.

What it actually looks like in reality is that you identify a high-priority market, say Kenya, for an East African expansion push, and begin the incorporation process. You appoint local directors, navigate the Companies Registry, register with the Kenya Revenue Authority, and open a local bank account to collect KES. You hire a local team or bring in a country manager who understands the market dynamics. You build relationships with local payment partners. Then, after anywhere from six months to two years of setup, you launch.

This model makes sense when you've already validated the market, when you have organic traction, clear demand signals, and unit economics strong enough to absorb the overhead of a permanent local structure. It's the right move for a Series B company entering its most important growth market, not a seed-stage startup trying to figure out if there's product-market fit in a new geography.

Incorporation in most African markets costs between $3,000 and $10,000 in legal and administrative fees, before you've hired anyone or acquired a single customer. Add local accounting, annual audits, tax filing software, and a country manager's salary, and you're looking at a significant fixed cost base that needs to be justified by proven revenue, not projected revenue.

Where the Merchant of Record fits

For companies pursuing direct market entry, an MoR like Startbutton can serve as a bridge, handling payments and tax compliance in the new market while the legal entity is being set up. This means you're generating revenue and learning about the market from day one, rather than waiting until the incorporation paperwork clears to serve your first customer.

2. The Traction-first approach: Test before you commit

This is the opposite of direct market entry. Instead of building local infrastructure before validating demand, you enter the market with minimal overhead, collect real data, and only commit to permanent structure once the numbers tell you to.

In reality, you have to identify two or three target markets based on organic signals, users signing up without paid acquisition, inbound inquiries from specific regions, or payment attempts from countries you haven't actively marketed to. You enable those markets through your payment infrastructure, localize your pricing, and start selling. You set a clear threshold, $10k MRR, 1,000 monthly active users, a 6-month retention rate above a certain benchmark, and you don't commit to incorporation until you've hit your goal.

This is the right model for early-stage companies and for established companies entering genuinely unfamiliar markets. It's also the model that most successfully avoids the single most common cause of startup failure: premature expansion. You're not betting on a market before you know it wants you. You're letting the market tell you whether the bet is worth making.

The primary cost here is speed, or rather, the ceiling on speed. Operating through a Merchant of Record without a local entity means you may have less control over the customer experience, and less access to local banking credit

Where the Merchant of Record fits

This is where the MoR model is most powerful. A Merchant of Record like Startbutton allows you to launch in a new market in 24 to 48 hours, no incorporation, no local bank accounts, no tax registration. Startbutton acts as the legal seller in the target market, handling VAT calculation, tax remittance, and compliance with local financial regulations and you get to collect in local currencyn or settle in USD, USDT or USDC, The most important advantage of all of these is that you get to spend your energy finding out whether the market wants your product, not building administrative infrastructure for a market that might not want what you are sellling.

3. Partnership and Reseller models

Instead of entering a market directly, you identify a local partner, a distributor, a reseller, or a strategic ally who already has the market relationships, the regulatory standing, and the customer trust you'd otherwise spend years building.

For instance, a Nigerian SaaS company expanding into Francophone West Africa partners with a Senegalese IT firm that already has enterprise relationships and government contracts. The partner sells the product under their existing relationships, handles local customer support, and takes a revenue share. The SaaS company provides the product, the training, and the technical infrastructure; both sides focus on what they're actually good at.

Partnership models work particularly well in markets where trust is built through local relationships rather than brand advertising, which describes most B2B markets across Africa. They also work well in markets where the regulatory environment is complex enough that having a local entity with existing compliance standing is genuinely valuable, not just convenient.

The honest cost implication is revenue share; you get to give up a percentage of every deal closed through the partner, which compresses your margins relative to direct sales. You're also giving up some control over how your product is positioned and sold, a meaningful trade-off if your brand narrative is central to your value proposition.

Where the Merchant of Record fits

No percentage of a deal is requested, and even in a partnership model, the MoR fully handles cross-border settlement, tax remittance, and local compliance. An MoR sitting beneath the reseller relationship ensures that the financial mechanics of every transaction are handled correctly, regardless of which entity is doing the selling. It also means you can expand the partnership model to multiple markets without rebuilding the compliance layer or the payment infrastructure each time.

4. Product-led growth across borders

Your product does the expanding for you. Users in new markets discover it, adopt it, and advocate for it before your sales team has made a single outbound call in that location.

This happens when a business has a valuable product built with the users in mind, for example, a B2B SaaS platform built in Lagos starts seeing signups from Nairobi, Accra, and Kigali without targeted marketing. Users share it within their professional networks. A free tier or trial converts organically. By the time the company formally decides to expand into these markets, they already have 500 paying customers there.

Product-led growth works when the product itself is the primary discovery and conversion mechanism, when it's easy to use, delivers clear value quickly, and has natural virality built into how it's used. Collaboration tools, productivity software, and developer platforms are classic PLG candidates. The model also works best when the product can be used without significant localization, when the core value translates directly across markets without heavy adaptation.

The risk with PLG international expansion is compliance lag. Your product is collecting revenue in multiple markets before your legal and tax infrastructure has caught up. In markets with Significant Economic Presence rules, like Nigeria and Kenya, where the tax obligation is triggered at a specific revenue threshold, creating a tax liability that arrives as a surprise during due diligence or a funding round.

Where the Merchant of Record fits

For PLG companies, the MoR model is the natural compliance infrastructure. As your product spreads organically into new markets, Startbutton ensures that every transaction in every market is handled with the correct local VAT, the correct currency conversion, and the correct regulatory framework automatically, without requiring your team to monitor tax thresholds across 15+ different countries in real time. While your product gets to grow freely, your compliance easily grows with it.

5. Acquisition and team buyouts

Instead of building market presence from scratch, you acquire it by buying a local company that already has the customers, the team, the regulatory standing, and the market knowledge you'd otherwise spend years developing.

A South African fintech expanding into Nigeria acquires a smaller Nigerian payments startup that has 200 enterprise customers, a CBN license, and a team of 30 people who understand the local market deeply. The acquirer gets instant market presence. The acquired company gets capital, product infrastructure, and regional scale.

Acquisitions make sense when speed to market is more valuable than cost efficiency, when a competitive window is closing, when a specific license or regulatory approval is the primary barrier to entry, or when the local team's relationships are genuinely irreplaceable. They also make sense when the target company has proven unit economics and a loyal customer base, rather than just a user count.

Acquisitions have their downsides because they are expensive, slow to integrate, and culturally complex. The majority of acquisitions underdeliver on their projected synergies. In African markets, specifically, the post-acquisition integration of payment infrastructure, tax compliance, and regulatory reporting across two previously separate entities can be genuinely complicated.

Where the Merchant of Record fits

During the integration period, which can last up to 12 to 24 months, an MoR provides a stable, compliant payment layer that doesn't depend on the integration being complete. Both entities can route transactions through the same infrastructure while the organizational, technical, and regulatory integration work happens in the background.

6. Multi-market expansion through Infrastructure orchestration

The most ambitious path is entering multiple markets simultaneously or in rapid succession, using a unified technical and compliance infrastructure rather than rebuilding for each market individually.

A digital commerce platform decides to go live in Nigeria, Kenya, Ghana, Rwanda, and South Africa within 18 months. Instead of incorporating in each country, they build on top of an MoR that already covers all five markets. One API integration, one compliance layer, settlement in local currencies, five markets, activated sequentially as the go-to-market team is ready for each one.

This model works for companies with a product that translates across markets without heavy localization, a clear pan-African vision that investors are backing, and the operational discipline to manage multiple market entry processes simultaneously without losing focus on product quality in any single one.

Speed across multiple markets simultaneously dilutes your team's attention and your ability to respond to market-specific dynamics. A problem in Kenya gets less focus when you're also managing launches in Ghana and South Africa at the same time. The companies that execute multi-market expansion successfully are usually the ones that have built extremely strong operational systems at home before they try to replicate them everywhere else at once.

Where the Merchant of Record fits

This is the use case the MoR model was built for. Startbutton currently covers 15+ African markets, meaning a single integration gives you legal selling capability, tax compliance, local payment rail access, and USD settlement across all of them. For a company with genuine pan-African ambitions, this is the infrastructure layer that makes the ambition executable, without requiring a legal team in every country or a compliance manager for every tax regime.

The through-line: Infrastructure determines pace

Every expansion model on this list moves at the speed of its underlying infrastructure. The fastest companies aren't the ones with the most aggressive growth targets; they're the ones who made the right infrastructure decisions early enough that expansion became a repeatable process rather than a one-time heroic effort.

The Merchant of Record model, and specifically Startbutton's implementation of it across African markets, doesn't replace the strategic thinking that good expansion requires. It removes the administrative ceiling that prevents that thinking from being executed quickly. No months of incorporation waiting. No compliance teams are spread thin across fourteen tax regimes. No currency trapped in local accounts. Just a compliant, settled, scalable payment layer that grows as fast as your GTM motion can push it.

The question for your business isn't which expansion model is theoretically best. It's which one your current infrastructure can actually support, and what you need to put in place to make the next stage of growth feel less like a gamble and more like a decision.

Read more

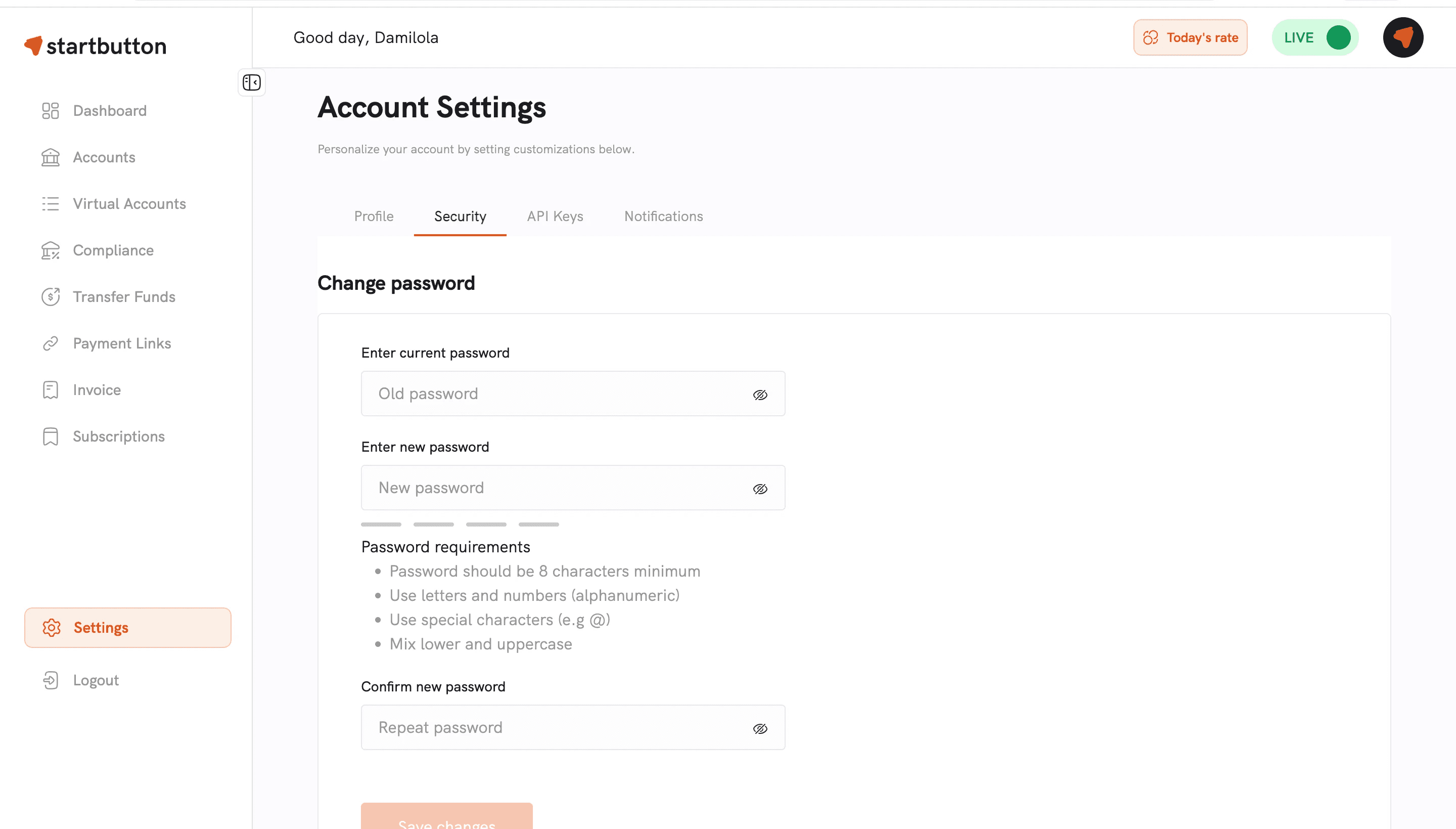

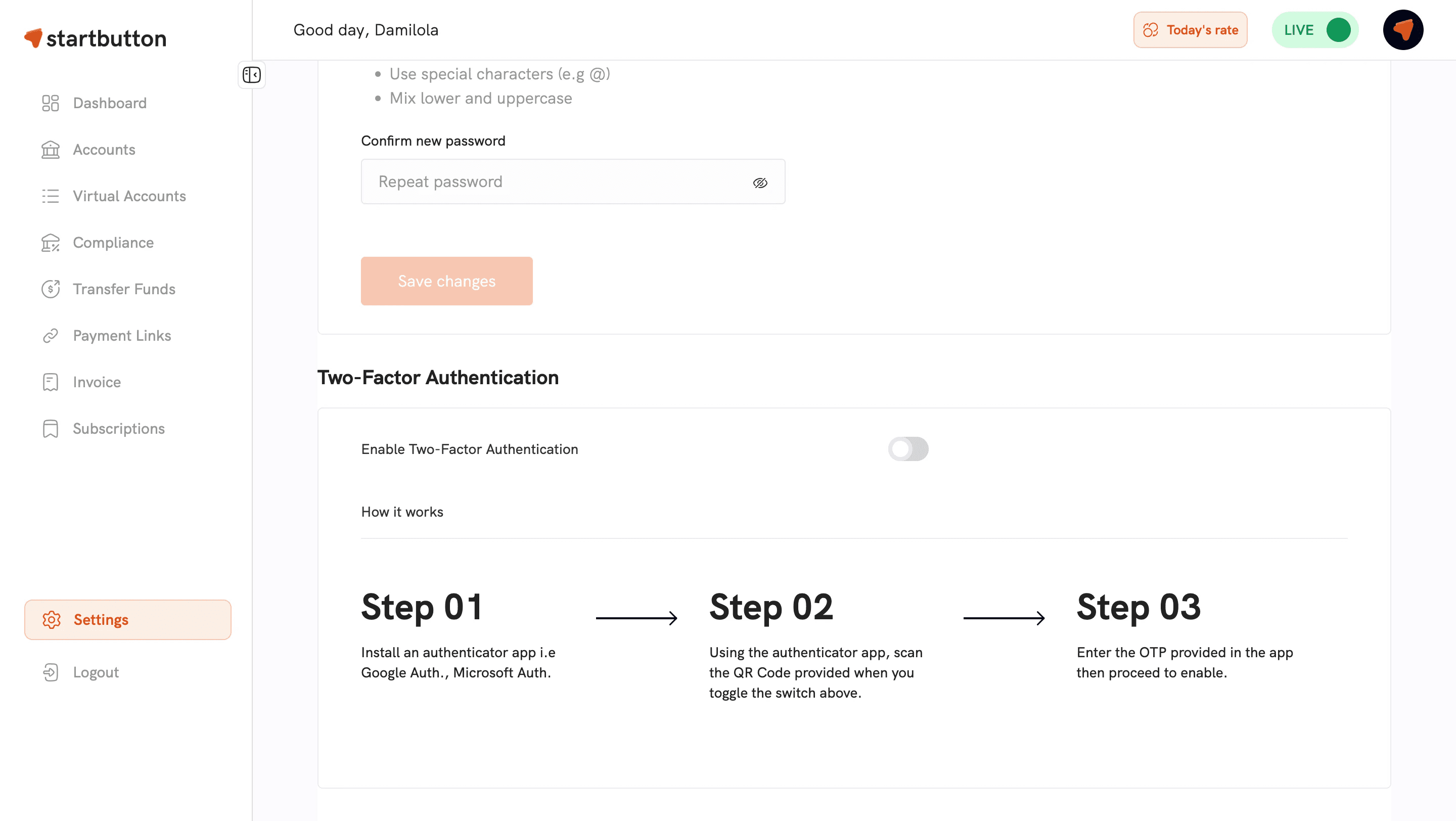

How to Enable Two-Factor Authentication (2FA) on the Startbutton Dashboard

Passwords are table stakes, but they're also the weakest link in account security. A strong password can be phished; a careful team member can still fall for a well-crafted scam—and once someone has your login details, they can access your dashboard and everything in it.

That’s why we built Two-Factor Authentication (2FA) for Startbutton.

Two-Factor Authentication (2FA) adds an extra layer of protection by requiring a second verification step in addition to your password when accessing the Startbutton dashboard, helping protect your account from phishing, password breaches, and unauthorized access.

What 2FA is

Two-Factor Authentication (2FA) is a security feature that requires two forms of verification before granting access to your Startbutton dashboard:

Something you know: your password

Something you have: a unique one-time code (delivered via a secure method, such as a code sent to your phone or generated by an authentication app)

This means that even if someone steals or guesses your password, they still can’t access your dashboard without the additional verification step.

Who can enable 2FA?

Merchant Admins

As a merchant admin, you have control over 2FA for your account and your team:

Set up 2FA for yourself to secure your own dashboard access.

Enforce mandatory 2FA for your entire team using an “enforce 2FA” control in the admin dashboard (or via API/endpoint).

Once enforcement is enabled, every team member must complete 2FA setup before they can access the dashboard.

Startbutton Admins (Eagle)

Startbutton admins can also enforce 2FA on a per-merchant basis via Eagle (internal admin tooling), so high-priority accounts can be protected when needed.

How it works for your team

When you enforce 2FA, here’s what happens

Team members receive an email notification instructing them to set up 2FA.

They log in with their email and password, then they’re guided through the 2FA setup flow.

They complete the setup by following the step-by-step instructions in the flow.

From that point forward, logins require both their password and the additional 2FA verification step.

Important: Team members cannot access the dashboard until they complete 2FA setup.

2FA is designed to strengthen account security, and it may also apply to high-risk actions such as transfers, where users may be prompted to enable or complete authentication before proceeding.

How to get started

Enabling 2FA is simple:

Log in to your Startbutton Dashboard

As an admin, locate the “Enforce 2FA” control in your admin dashboard settings (or enable it via API/endpoint).

Save/confirm your change

Once enabled, your team will receive email instructions and be guided through the setup process when they sign in.

Frequently asked questions

What happens if a team member has trouble setting up 2FA?

They can reach out to you (the admin) or contact our support team at support@startbutton.africa.

Can I disable 2FA after enabling it?

Yes. Merchant admins can enable or disable 2FA enforcement at any time from the admin dashboard or via API/endpoint.

Is 2FA required for anything else besides login?

2FA is primarily for securing dashboard access. It may also be required for certain high-risk flows, such as transfers, depending on your account/security configuration.

Can I set up 2FA for myself without enforcing it for my team?

Yes—admins can set up 2FA for themselves, and separately decide whether to enforce it for the entire team.

What if I lose access to my 2FA method?

Contact support at support@startbutton.africa for assistance with safely restoring access.

Ready to enable 2FA?

Head to your dashboard admin settings and turn on Enforce 2FA to secure your account and your team.

Read more

Accepting Credit Cards and Mobile Money in Nigeria, Ghana, and Kenya

A reality check most payment guides won't give you upfront: Africa doesn't have a payment problem, it has a payment complexity problem, and trust that there's a meaningful difference between the two.

Mobile money penetration in Kenya hit 91% in 2025, Nigeria processed NGN 1.56 quadrillion in electronic transactions in the first half of 2024 alone, and Ghana recorded its highest-ever monthly mobile money volume, GH¢ 518.4 billion, in December 2025. These aren't emerging markets dipping their toes into digital commerce. They're live, high-volume economies with sophisticated payment rails and consumers who transact digitally every single day.

The problem is that each market runs on different infrastructure, different regulations, and different consumer behaviors, and navigating all three simultaneously, without the right architecture underneath you, is where most foreign businesses quietly fail.

This is a guide to doing it right.

The first decision that determines everything else

One foundational decision you need to make before anything else is to determine if you are going to be the legal seller in each market, or if you are going to work with someone who already is.

This is the difference between a Payment Service Provider (PSP) and a Merchant of Record (MoR), and it's not a subtle distinction.

A PSP like Paystack or Flutterwave is a technical gateway. It moves money efficiently and provides solid APIs. When you use a PSP, you remain the legal seller; that means you own every tax obligation, every VAT filing, every chargeback dispute, and every compliance requirement in every country where your customers live. For a business with a local entity, a dedicated finance team, and established relationships with local tax advisors, that's manageable. For a business trying to move fast across three markets simultaneously, it's a full-time operational burden that has nothing to do with your product.

A Merchant of Record like Startbutton steps in as the legal seller on your behalf. When a customer in Lagos or Nairobi makes a purchase, the MoR is the entity that appears on their bank statement, handles the tax calculation, remits VAT to the local authority, and assumes liability for fraud and chargebacks while you stay focused on the growth of the product. The MoR handles the regulatory infrastructure that sits around every transaction.

PSP | Merchant of Record | |

Legal Seller | Your business | The MoR |

Tax responsibility | You calculate and remit | MoR handles everything |

Setup time | Weeks to months | 24–48 hours |

Chargeback liability | Your problem | MoR's problem |

Local entity required | Usually | You have to be registered in a country |